Vogue magazine names Wizkid the hottest African pop star by any measure after the afro beats sensation, unveil a Merch Capsule New York.

According to the U.S. Department of Agriculture, it will take roughly $240,000 to raise a child from birth to age 18. For a special needs child, those expenses can quadruple. – Craig Guillot, The Cost Of Raising A Special Needs Child, Mint.comFurther, the financial requirements for many special-needs children do not stop at age 18. Many will be unable to live independently. Parents need to financially plan for the longterm future for their child.

A quarter of U.S. households have a member with special needs. More than 8% of kids under 15 have a disability, and half of those are deemed severe. – Jeff Howe, Paying For My Special-Needs Child, TimeWhen it makes sense: Survivorship life insurance polices are an excellent option for parents to financially plan for their special-needs child, even after both parents have passed away.

It pays to shop around to see which insurer offers the best price for specific circumstances. And instead of working with a broker exclusively affiliated with a single insurer, work with an independent agent who has access to the top term insurance providers. –

Accelerated underwriting is perfect for anyone that wants life insurance with the least amount of hassle. It is important to note that currently you will still find that fully underwritten policies will offer more competitive term life insurance quotes. However, often the difference in pricing between accelerated underwriting vs fully underwritten life insurance is minimal and worth the few extra dollars for the ease of getting the coverage.Why would I choose accelerated Underwriting?

Eligibility for accelerated underwriting typically comes down to a few primary criteria. Most policies require that the applicant be between 18 and 50, although some companies offer accelerated underwriting up to age 65.Am I eligible for accelerated underwriting?

The process consists of talking with an agent familiar with accelerated underwriting companies. After you work with your agent to fill out an application, it is then submitted to the carrier of choice. Some carriers conduct a further telephone interview, while other companies simply run a quick background check. It all comes down to the company you apply with and what that company’s criteria is going to be.How do I get an accelerated underwriting life insurance policy?

Banner Life

Banner Life  The Future of Life Insurance

The Future of Life Insurance

Here is the ultimate truth about life insurance: the only policy that matters is the one that is in force on the day you die. – Tom Hegna, economist, author, retirement expertTom Hegna’s quote is powerful. If you have loved ones who would suffer financially should you pass away, you need a life insurance policy that is in force.

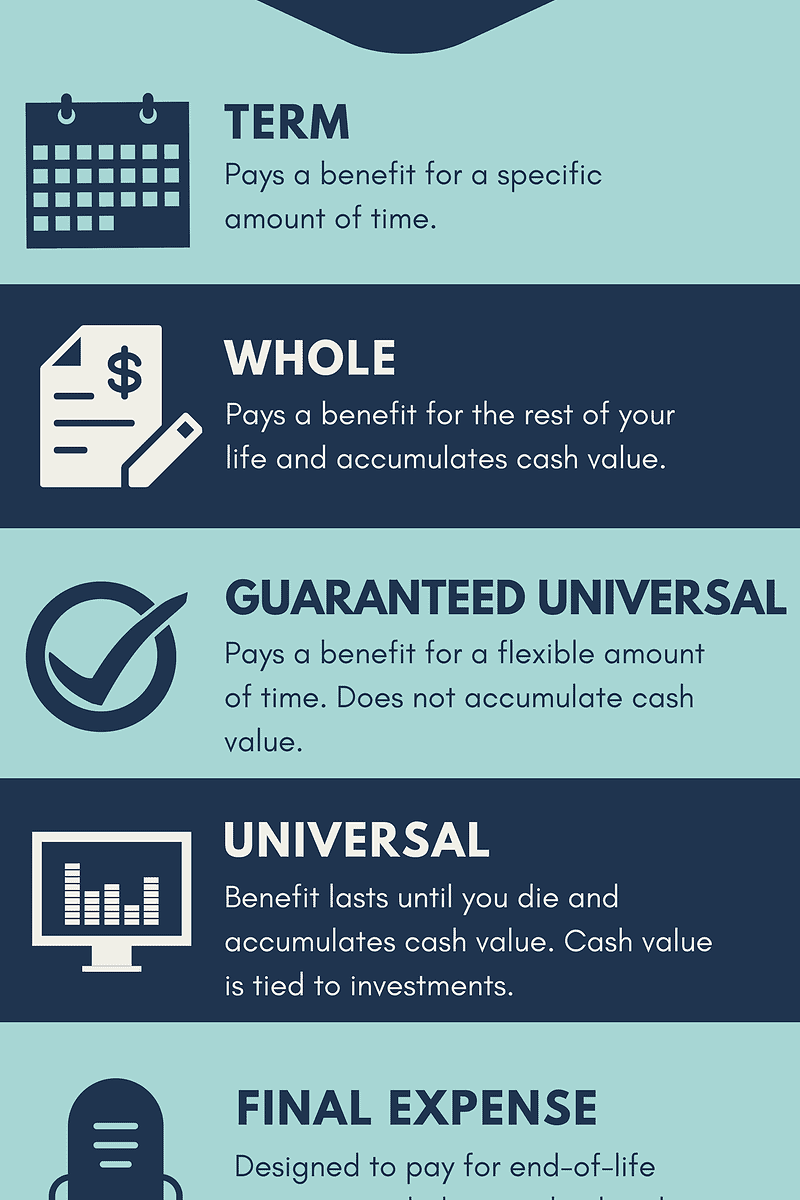

Cash values, which accumulate on a tax-deferred basis just like assets in most retirement and tuition savings plans, can be used in the future for any purpose you wish. If you like, you can borrow cash value for a down payment on a home, to help pay for your children’s education or to provide income for your retirement. When you borrow money from a permanent insurance policy, you’re using the policy’s cash value as collateral and the borrowing rates tend to be relatively low. And unlike loans from most financial institutions, the loan is not dependent on credit checks or other restrictions. You ultimately must repay any loan with interest or your beneficiaries will receive a reduced death benefit and cash-surrender value. – Permanent Insurance, Life Happens, a nonprofit life insurance awareness organizationWhole life insurance has some main characteristics:

30.3 million Americans, or 9.4% of the population, has diabetes. Approximately 1.25 million American children and adults have type 1 diabetes. – American Diabetes AssociationWhile medical advances on treatment and prevention continue, those of us with the condition can attest that it’s difficult to live with.

I went to the doctor and he said, ‘you know those high blood pressure levels you’ve been dealing with since you were 36? Well you’ve graduated, you’ve got Type 2 Diabetes, young man. – Tom Hanks, appearing on the David Letterman ShowNo doubt, diabetes, whether it’s type 1 or type 2, adds a layer of complication to your life.

It used to take at least a couple of weeks to get approved for a life insurance policy. Now, with online tools, it can take a couple of minutes. – Jean Chatzky, Everything You Need To Know About Shopping For Life Insurance Online, NBC NewsLife insurance companies realize that a percentage of the population has no interest in being poked with a needle. Technological advances and database systems opened the door for a multitude of no exam life insurance products.

| $1,000,000 | ||||

|---|---|---|---|---|

| 10 Year | 15 Year | 20 Year | 30 Year | |

| 30 Year Old Male | $24.50 | $28.88 | $38.50 | $64.48 |

| 40 Year Old Male | $29.75 | $40.25 | $55.56 | $103.69 |

| $1,000,000 | ||||

|---|---|---|---|---|

| 10 Year | 15 Year | 20 Year | 30 Year | |

| 30 Year Old Female | $21.00 | $27.30 | $32.16 | $54.38 |

| 40 Year Old Female | $27.56 | $36.75 | $46.81 | $83.13 |

Life insurance is one of the pillars of personal finance, deserving of consideration by every household. I’d even go so far as to say it’s vital for most. – Tim Maurer, 10 Things You Absolutely Need To Know About Life Insurance, Forbes

How can I afford long term care?

Example: Samantha is 25-years-old female in good health. She is able to purchase $250,000 20-year term insurance for as little as $13.78 per month.

Tim is 45-years-old male in average health. A 20 year term policy for $250,000 will cost him about $77.65 per month.

We wanted to list Myths 6 and 7 one after another to stress that everyone has different life insurance needs. Therefore, you can’t group all insurance policies and say that one is always better than the other. When shopping for life insurance, it is important to know why you need the coverage. This will help you find the best product for YOU. Do not fall for these one-size-fits-all myths.

Get Health Wise Copyright © 2010 Blogger Theme is Designed by Lasantha